Original Question: Are e-wallets permissible? And do we need to perform zakat for money in e-wallets?

Money and payment methods have evolved significantly with advancements in technology and digital finance. Today, electronic wallets (e-wallets) have emerged as a widely used payment instrument that allows users to store and transact using electronically stored monetary value linked to existing fiat currencies such as Singapore Dollars and Malaysian Ringgits.

E-wallet stores e-money, and e-money functions as a digital representation of fiat money issued and managed by licensed providers. The value stored in an e-wallet represents the issuer’s obligation to redeem it with the corresponding fiat currency, making it primarily a modern payment mechanism rather than a separate independent currency. As such, e-wallets are generally viewed as a technological medium facilitating payments, transfers, and financial transactions in a more convenient and efficient manner. It serves as a payment method for products and services by merchants, and users can transfer funds via peer-to-peer (P2P) services. Over the last decade, developments in mobile technology such as Quick Response and mobile applications have resulted in significant growth in e-money, with a transition from traditional stored value cards to online accounts and e-wallet.

There are numerous types of e-wallets available in Singapore, many of which are commonly used in daily transactions. According to the Singapore Computer Society, some of the most popular e-wallets in Singapore include GrabPay, FavePay, DBS PayLah!, Singtel Dash, and EZ-Link Wallet

In this regard, it is notable that MAS explains on the different modes of payment such as e-wallet: “A payment account may take the form of an e-wallet which is funded with e-money. This e-money is denominated in or pegged by the issuer to a fiat currency“. It further elaborates that e-money is different from deposits: “E-money is money paid in advance under a contract for the provision of a service. E-money are not bank deposits and therefore not protected by deposit insurance.”

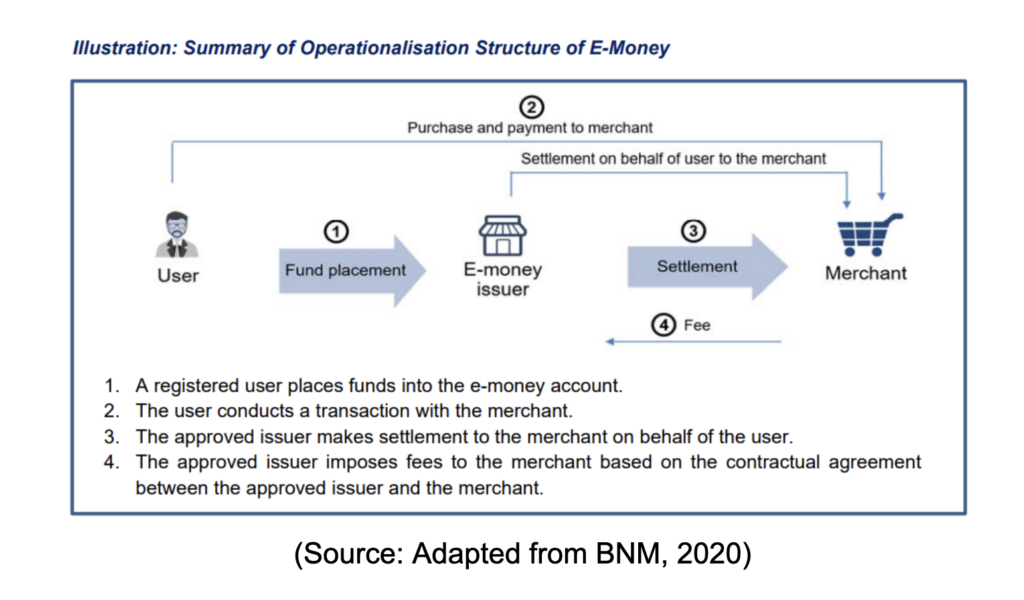

From a Shariah perspective, the agency contract (Wakalah) is used when the issuer acts as an agent to make payment on behalf of the user to the merchant and the funds deposited may be considered as a loan (Qard) from the user to the issuer. Below is a summary of the operationalisation of e-money.

In this regard, the Shariah Advisory Council (SAC) of Bank Negara Malaysia (BNM) in its 201st meeting in January 2020, resolved that e-money is a permissible payment instrument under Shariah. The ruling is based on the understanding that modern technology and digital platforms merely function as tools facilitating commercial transactions in a more efficient and convenient manner. Similarly, International Islamic Fiqh Academy (Majmaʿ al-Fiqh al-Islāmī) recognises the validity of conducting transactions through modern communication technologies and digital devices, as these technologies are generally treated as neutral mediums for payment and exchange.

This position is consistent with the established fiqh legal maxim:

“The original ruling of matters is permissibility.”

Therefore, IFSG concludes that e-wallets are generally permissible as they function as a payment method and a store of value, not an interest-bearing instrument. The permissibility remains as long as there is no riba paid on the balances, funds are not automatically invested in Shariah non-compliant activities, and the e-wallet is used for halal transactions.

Furthermore, e-money in e-wallet are considered as cash. Therefore, zakat requirements still applies. If the combined total of one’s cash (physical cash, bank balance, e-wallet, other liquid instruments) reaches the nisab and one lunar year (hawl has passed), zakat of 2.5% would be obligated on the balance.

And Allah knows best.

Reference:

- https://www.bnm.gov.my/documents/20124/943361/27012025_Revised_E-Money_PD_v2.pdf

- https://muzakarah.inceif.edu.my/kertas-kerja-slide/Sesi%203%20-%20Isu-isu%20Syariah%20-%20BNPL,%20e-Wallet%20(Ust%20Munawwar).pdf

- https://www.bnm.gov.my/documents/20124/914558/03_SAC201_Statement_eMoney_en.pdf

- Qarar Majma` Fiqh al-Islami, 6th Mu`tamar, 14 – 20 March 1990, Jeddah

- Radzi, R. M., Ramli, W. N. W., Rahmawati, L., & Tantriana, D. (2024). E-wallet transaction framework in Malaysia: an evaluation of potential shariah issues. International Journal of Religion, 5(6), 986-996. (https://pdfs.semanticscholar.org/0775/3ae4228f010c23c1aa6093e734f5279608be.pdf)

- https://www.mas.gov.sg/contact-us/faqs/payments-faqs/payments-service-licensing-faqs

- https://www.imf.org/-/media/files/publications/dp/2021/english/empsoupea.pdf

- https://www.scs.org.sg/articles/e-wallet-singapore